Earnings misses recall recession-like numbers, pressure stocks

Stocks came under pressure after the European Central Bank hinted its intent to cut interest rates for the first time since early 2016.

Investors are taking the news as a sign that the global economy is slowing down and needs a new easing cycle to regain momentum.

The ECB also signaled it could possibly restart its giant bond-buying program in a policy shift aimed at back-stopping the eurozone economy.

The move comes as the Federal Reserve is set to cut rates for the first time in a decade next week, while central banks in Asia and South Africa lowered their borrowing costs earlier this month.

ECB President Mario Draghi signaled that looser policy was likely to follow if inflation continues to disappoint.

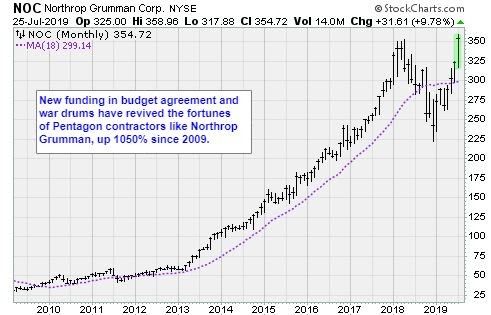

The impact on stocks was notable: Breadth favored decliners by a 3-1 margin, and there were 291 new one-year highs vs 170 new lows. Topping the new high list and finishing in the black were Northrop Grumman (NOC), Blackstone (BX), Sherwin-Williams (SHW), Baxter International (BAX), and Hershey (HSY). Cats and dogs.

Speaking of “cats” …

Caterpillar (CAT), along with Boeing (BA), dashed the run of strong profit reports that had supported major indexes’ gains earlier in the week. Their disappointing reports reminded investors that many companies, especially multinationals, are coping with a challenging economic environment.

The dangers are not as evident in the U.S., so the global troubles are being mostly ignored for now. But they are still having an impact on the overall numbers …

- Caterpillar shares fell 4.5% after it reported lower sales in China and higher costs due to tariffs and labor. The company said the tough economic climate isn’t expected to abate, guiding its full-year profit to the lower end of its forecast.

- Boeing said it lost $2.94 billion in the June quarter, its biggest loss ever, due to the grounding of the 737 MAX jetliner.

This is serious. Earnings appear to have entered recession territory, and that is likely to persist.

At best, earnings will rebound late next year, leaving markets vulnerable to volatility in the meantime.

Global Economic Data Weakens

Now let’s dig a little deeper on the fundamental front.

Markets responded indifferently to weak Purchasing Managers’ Index data on Wednesday. This was a manifestation of investors’ remarkable complacency about the outlook for the global economy and corporate earnings.

- The eurozone composite PMI for July fell more than anticipated. It is now in a state consistent with very weak economic growth (of 0.2% quarter-over-quarter) in the region, according to Capital Economics research.

- While the U.S. composite PMI rose a touch, the data still points to a sharp slowdown in growth. The calm in equity markets arguably reflects the overly optimistic view embodied by the IMF’s World Economic Outlook. The consensus is that the global economy will pick up soon, helped by looser monetary policy.

This suggests that the chances of a major disappointment on the earnings front are high. Capital Economics analysts observe that even mild slowdowns in the global economy in the past have coincided with much greater weaknesses in corporate earnings than the consensus currently anticipates.

Anything less than a rapid rebound in the global economy, CapEcon argues, will probably result in weaker earnings than the consensus expects. That, in turn, will probably cause global equities to struggle the rest of the year.

This contraction of corporate income is no joke …

“We need to see a pretty big improvement in corporate earnings to justify any further price appreciation from where we are right now,” said the highly respected Sam Stovall, chief investment strategist at CFRA Research.

The market often peaks for the summer in the third or fourth week of July. Prices always move before the news, so we should know soon enough what the catalyst will be.

The catalyst that will lead to the market’s next move will probably not be any of the “known knowns” like the U.S.-China trade deal (or lack thereof) or Washington politics. It will probably be something more obscure this time. Maybe a blow-up of Deutsche Bank (DB), a new escalation of the Iran conflict, or continued economic breakdown in China.

If the market significantly falters over the next few months to a year, we will see another great opportunity to buy stocks essential to the growth of the future economy. Names like Microsoft (MSFT), Amazon (AMZN), Alphabet (GOOGL), Salesforce.com (CRM), Northrop Grumman (NOC) and select utilities.

My Tech Trend Trader subscribers are sitting on some pretty nice gains in some of these names, and plenty more just like them. Be among the first to get my picks — on both the buy and the sell side — when you take my service for a test-drive. You can get on board here.

***

Budget Deal Breaks the Bank

The two-year budget deal in Washington between the White House and Congress this week removed uncertainty over the debt-ceiling fight. It also massively added to debt risk.

The market doesn’t really have to adjust, since the pact was expected. But it practically locks in lower GDP growth for next year — perhaps checking in as low as half of this year’s likely rate of around 2.3%.

The $320 billion increase in spending agreed by Congress sounds like a lot of money. But it will be spread over two years and refers to the increase relative to the originally planned cap level rather than the change from the previous year.

In reality, a CapEcon analysis shows the spending cap will increase by a modest $50 billion in 2020 relative to 2019, equivalent to only 0.2% of GDP. And then it would remain at roughly the same level in 2021.

The deal also includes around $75 billion in projected cost savings. But those aren’t due to take effect for several more years.

CapEcon observes that the ease with which this two-year budget deal was concluded illustrates that the fiscally conservative Republicans have lost what little influence they had with the president.

The federal budget deficit has more than doubled since 2016 and is on course to exceed $1 trillion next year. Since the economy is close to full employment with an unemployment rate below 4%, that demonstrates a complete breakdown of fiscal discipline.

Spending has continued to rise in line with its long-run trend. But the tax cuts introduced at the start of last year have prevented revenues from rising more substantially.

Corporate tax revenues are still lower than they were at the start of 2018. For now, the markets don’t see this as a problem, as the 10-year Treasury yield is barely above 2%. However, the bond market’s views can change quickly and viciously, so beware.

Best wishes,

Jon D. Markman

Some news and research provided by Wall Street Journal, Bloomberg, Associated Press, Reuters and Capital Economics.