Markets pole-vault a steadily rising wall of worry

Stocks mostly drifted higher over the past week like snowflakes shifted into reverse, as investors were amused by the latest White House promise that trade talks with China were going swell and entering their final phase. Again. Maybe.

Advancers outpaced decliners all week by a 3-to-2 margin. Yet, through Thursday, there were just 149 new one-year highs vs. 58 new lows. That’s a really low number of new highs for such a strong up day, which is unnerving.

Leading the pack were oddballs Comcast (CMCSA), Ecolab (ECL), Amphenol (APH), O’Reilly Automotive (ORLY), Hilton Worldwide (HLT) and Lululemon Athletica (LULU). Strange bunch.

I really wonder about the future of cable providers like Comcast. Recently, I finally got tired of writing a $400 check to Comcast for internet, TV and phone service at my office every month and made an end run.

I canceled my internet service and bought a MiFi device from Verizon instead that will bring me similar speeds for about a third of the price. Then I dumped Comcast’s TV service and replaced it with YouTube TV at $40/month, which is less than half the Xfinity price.

This cord-cutting stuff is getting real. My goal is to only pay for the internet and TV service that I actually use, more or less on a metered basis. Like cars that sit idle most of the time in your driveway and office parking lot, yet continue to rack up insurance costs and depreciation, most of the time I am not working online or watching television. My office day is around 8 a.m. to 4 p.m., or 9 hours, five days a week. That’s 45 hours. Yet I was paying for 168 hours of service.

I’ll let you know how my Comcast revolt goes. And hang on, because 5G service — which is coming later this year or early next — will be another game-changer.

It will allow the Verizons and T-Mobiles to provide sizzling broadband speeds over the air, compromising Comcast’s heavy cable and wired business.

Speaking of compromise …

*

Progress on U.S.-China trade talks and caution from central banks around the world this week have eased fears of a far-reaching economic slowdown. This has served to support stocks and other risky investments.

Equity market advances midweek came after the Financial Times reported the U.S. and China have resolved most of the sticking points that were preventing an agreement to end their tariff dispute.

Some investors expect an agreement will lift the outlook for the global economy, while others suspect it will lead to a “sell the news” event after months of advance on the rumor it could happen.

*

Materials shares tied to the health of the economy have been among the market’s best performers, with the S&P 500 materials sector (XLB) leading the way. Makers of semiconductors reliant on trade flows and Chinese demand also surged, with shares of Micron (MU) jumping 4% on Wednesday alone — providing our Strategic Options service subscribers with a quick 70% tracked gain in the May calls.

One of the big economic headlines of the week was a drop in the ISM non-manufacturing index to a 20-month low in March. The news adds to the message from the incoming hard activity data that underlying U.S. demand growth is slowing.

With the government policy mix much less favorable this year, Capital Economics analysts expect economic growth to remain below its 2% potential pace.

The fall in the headline Institute for Supply Management non-manufacturing index to 56.1 from 59.7 was driven by sharp declines in the business activity index, to 57.4 from 64.7, and the new orders index, to 59.0 from 65.2.

That said, the headline index is still far from recessionary levels, and is consistent on past form with solid GDP growth of around 2% annualized.

I suspect it will be worse than that; more like 1.5%.

Jack Albin, chief strategist at Cresset, is a little more optimistic, though not abundantly so. He believes that data shows the U.S. economy is slowing but is expected to outpace “stall speed.” GDP grew 3.1% last year, its best calendar-year showing since 2005. Economists credit a powerful blend of monetary accommodation and an unprecedented corporate tax cut for this expansion.

While lawmakers hoped the incentives would fuel a self-perpetuating investment renaissance, “initial indications suggest the legislation simply provided a booster shot,” says Albin. Now, it appears the medicine is wearing off and the U.S. economy is downshifting toward its longer-term 2% trend growth rate.

Stocks don’t care for now, but stay on your toes because sometimes the realization happens late and suddenly, like Wile E. Coyote running off a cliff and hanging in the air for a few beats before gravity takes over.

*

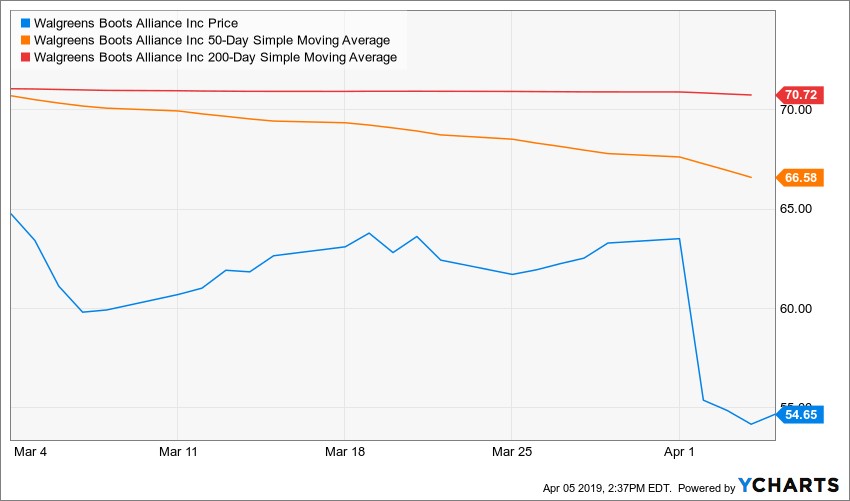

The most interesting stock news of the past week was the sharp 14% tumble taken by Walgreens (WBA). The big drugstore chain said it faced its most difficult quarter since its 2014 acquisition of Alliance Boots.

The retailer fell short of analysts’ profit expectations for the latest quarter and warned that challenging economic conditions, including falling generic drug prices, will weigh on earnings throughout the year.

Walgreens is no tech hotshot with an uneven earnings stream. Rather, it’s like a utility where you can buy aspirin, milk and Halloween candy. Companies like this are supposed to be slow, steady and largely bulletproof. So, it’s no wonder that investors worry Walgreens could be at the beginning of a rough earnings period.

S&P 500 companies are projected to report a 4% profit contraction from a year earlier, the broad index’s first quarter of negative earnings growth since 2016. Profit estimates for subsequent quarters continue to fall, raising the likelihood of an earnings recession.

Some investors and analysts say estimates for subsequent quarters this year likely need to come down further to reflect the rough economic terrain companies like Walgreens have warned about.

*

Adding to investors’ economic trepidations was a drop in orders for long-lasting factory goods in February following three straight months of growth. A sharp decline in civilian aircraft orders contributed to a 1.6% pullback in orders for durable goods in February from January.

Even putting the volatile aircraft order shortfall aside, analysts at Capital Economics note that orders were muted, reflecting the recent deterioration in global manufacturing activity.

The decline in commercial aircraft orders was largely as expected since investors already knew that Boeing received orders for only five planes last month, down from 46 the previous month.

With the 737 line accounting for 60% of Boeing’s orders, this will weigh on the durable goods data over the coming months.

Excluding transportation, core orders increased by only 0.1% month over month, with the weakness widespread. Non-defense capital goods (ex-aircraft) shipments are on track to expand by a modest 4% annualized in the first quarter. CapEcon observes that with consumption growth unusually weak, it’s fair to estimate that first-quarter GDP growth was a modest 1.5%.

As noted a moment ago, so far the equity markets don’t seem to care, possibly because investors choose to look through the trough to a rebound on the other side, and are focused instead on accommodative interest rate policy at the Federal Reserve and low inflation to counterbalance the negatives.

Best wishes,

Jon D. Markman