Stocks shot to new record highs over the past week.

Record highs are scary to some people, as those smack of complacency and overconfidence. But new highs are the most bullish things that can happen to stocks.

(If you’re riding out the correction in cannabis stocks and have questions about it, email them to my colleague Sean Brodrick right away. He plans to answer them at a special Q&A event this coming Monday, June 24. Plan to join him online here at 2 p.m. Eastern (11 a.m. Pacific).

And the way we have gotten here — a circuitous path through an awful May and many bumps in early June — has not actually built up an overbought condition. Rather, it’s been like walking through a park with lots of twists in the path that have added color and variety to the excursion, but not exhaustion.

Breadth has been positive but not extreme, at 5-3 in favor of advancers over the past week. On Thursday there whopping 866 new one-year highs vs 125 new lows.

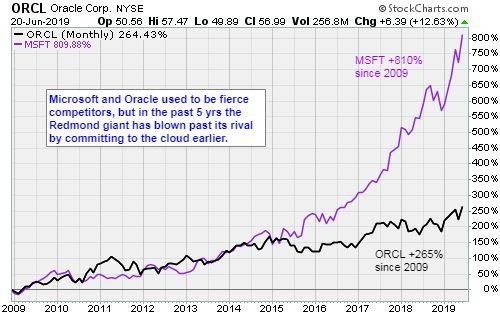

Topping the new high list were Microsoft (MSFT), Visa (V), Novartis (NVS), Oracle (ORCL), Abbott Labs (ABT), Adobe (ADBE), Costco (COST), Danaher (DHR), Lockheed Martin (LMT), Stryker (SYK) and S&P Global (SPGI).

The rebound comes after trade tensions and uncertainty over central-bank policy rattled investors last month, with stocks posting their worst May since 2010. But the potential for thawing trade relations between Washington and Beijing — along with central bank hints of lower interest rates ahead — have helped lift share prices this month.

The S&P 500 is on pace for its best June since 1955.

Fed chief Jay Powell said Thursday that the bank will hold interest rates steady for now, but he winked that further easing would be necessary if global trade tensions continue to dampen economic growth.

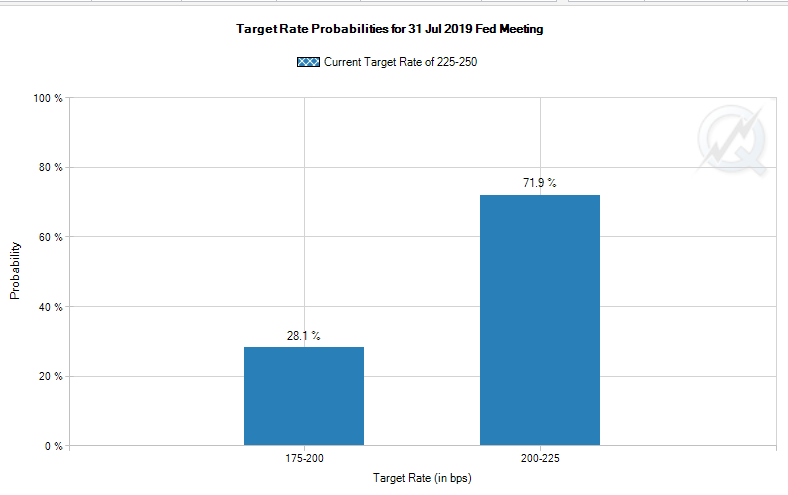

Most economists expect the Fed to propose a 25-basis-point cut at its July meeting, though some have made the case for a “go big or go home” 50-bp cut.

Image credit: CME FedWatch Tool

The recent bounce in stocks comes as President Trump is set to meet with Chinese President Xi Jinping at the Group of 20 summit next week in Japan. Both leaders have a lot at stake, and investors are starting to bet on the potential for compromise.

Late Thursday came word that the White House ordered airstrikes on Iran, then called them off. In my experience, overseas combat is one of those things that logically should irritate investors but historically has been a non-factor. Who can forget the night of “shock and awe” over Iraq in March 2003 that initiated a massive, bear-market-ending rally?

At the risk of sounding overly glib about a serious subject, wars destroy a lot of stuff that must then be replaced … at someone’s profit.

***

The Curious Case of The

Missing Individual Investor

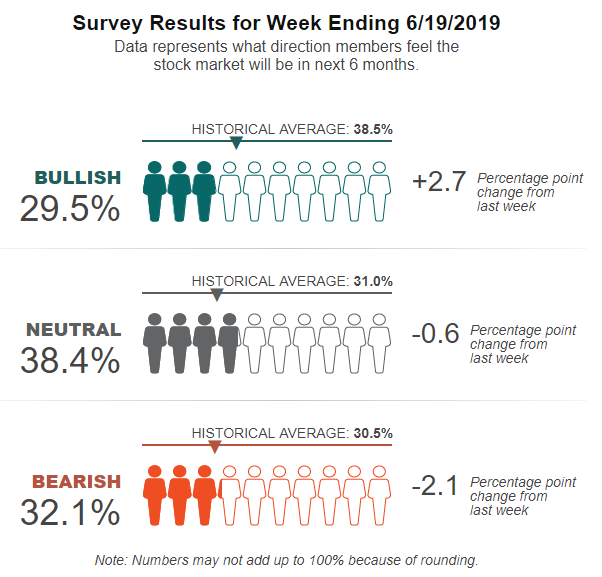

Several times over the past month, sentiment analyst Jason Goepfert has looked at the curious case of the missing individual investor.

Despite a relatively healthy market, he notes, respondents in the AAII survey have been increasingly pessimistic. That has been a very good sign in the past and looks to be following through yet again.

This week, investors started to change their opinions a bit, but bears still outnumbered bulls in the AAII survey. That’s curious because the day after the survey closed the S&P 500 blasted to a record high.

Goepfert riffed his database to find every time the S&P 500 hit a new multi-year high and the latest AAII reading showed more bears than bulls. It’s very unusual; there are only four precedents in the past 30 years.

Turns out there was very little risk in stocks after these signals. At no point over the next year did the S&P 500 lose any more than 4.6%, while it gained more than that at its best point every time.

The average two-month gain has been 4.7%; six months, 7% and 12 months, +20% with no losses. The last one was signaled on May 5, 1997, and the 1-year follow-on gain was 34.4%.

Bottom line, according to Goepfert: Such low optimism from this normally ebullient group of investors has been a consistently good sign, especially when it occurs during a healthy market.

***

Fed Prepares to Cut Rates Vigorously

Now let’s dig in on the Federal Reserve’s assessment of the U.S. economy and its outlook. I’m relying on the excellent analysis of the boutique research shop Capital Economics.

In its post-meeting statement Wednesday, the Fed confirmed that it is leaning toward interest-rate cuts later this year.

While many investors are looking for cuts to start in July, Capital Economics analysts believe that the initial rate cut will be delayed until September, with another 25-basis-point reduction coming in December, and then a final cut in March next year.

The Fed dropped its “patient” stance from its statement. It indicated instead that, in light of the increase in “uncertainties” surrounding the economic outlook and muted inflation, it will “closely monitor” the incoming information and ” act as appropriate to sustain the expansion.”

The current assessment was toned down only slightly: Economic growth was described as “moderate” rather than the previous “solid.” But that was to be expected since most forecasters believe GDP growth will be around 1% to 2% annualized in the second quarter. (Which is down from 3% in the first.)

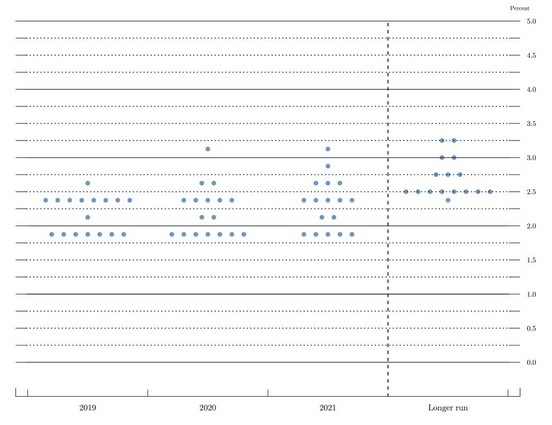

Despite the weakness in May’s payroll employment, job gains were still described as “solid.” As for the Fed officials’ economic projections, widely known as the “dot plot,” GDP growth forecasts were left almost completely unchanged and the core inflation projections were revised down only trivially below 2%.

This illustrates that the case for rate cuts is almost entirely a response to rising downside risks.

Fed officials now think the current stance of policy is close to neutral. The median interest-rate projection still shows interest rates unchanged at 2.4% this year, albeit then falling to 2.1% in 2020. But those median projections mask a big split …

Seven officials expect 50 bp of cuts this year, one anticipates one 25-bp cut, eight expect no change in rates and one forecasts a 25-bp hike.

Nevertheless, this is the first time since the projections began in 2012 that the median rate forecast shows any sort of decline whatsoever, with a majority of officials expecting rates to fall in 2020.

Not one of the 17 officials expect more than 50 bp of rate reductions over the next few years.

CapEcon notes that this should have come as a disappointment to futures markets, which had 100 bp of cuts by end-2020 fully priced in before the meeting, with a close to 100% chance of a 25-bp cut in July.

The reality, however, is that the Fed’s modest dovish shift has encouraged speculation of an even bigger policy loosening. After the announcement, futures markets began to price in a modest chance of a 50-bp cut in July and 75 bp of loosening by the end of this year!

In his press conference, Powell noted that even those officials who didn’t forecast rate cuts this year were at least open to the possibility. Although, at the same time, he acknowledged that there was “not much support” for a rate cut today.

Bottom line: The Fed is waiting to see what the incoming data bring. It’s fair to expect the data to continue weakening, but perhaps not quickly enough to warrant a rate cut as soon as next month, particularly if the G20 leaders’ meeting triggers a new round of trade talks between the US and China. I suspect those talks will fail without a deal, but their temporary resumption would point to the first rate cut being delayed until September.

That’s actually a bullish scenario for stocks.

An accommodative Fed, coupled with low inflation, moderate growth and accommodative stances in Japan, the eurozone and China, is collectively a recipe for a market melt-up, or at least a very risk-on climate.

It can always get screwed up by policy mistakes from the White House, but there is always going to be something to worry about.

And just so you know, some big money is upping the ante:

Goldman Sachs analysts flagged the possibility of a 50-bp cut in July if there is a big disappointment in the economic data, or if members want to get ahead of the curve, between now and then.

Best wishes,

Jon D. Markman