Sony Could Check Out Big Profits with this Grocery Grab

The Internet of Things is a topic I’ve touched on several times before. Like in this issue. And this one. It’s one of the four most profitable megatrends that will influence not just the next year, but the next decade.

Dr. Martin Weiss’ 2020 Preview: Megatrends and Megaprofits video details all four of those megatrends PLUS six surprising forecasts that will help you prepare for the coming decade.

Martin also gave away our editor’s top picks — seven specific recommendations from Tony Sagami, Sean Brodrick, Mike Larson and me — from our most expensive research services.

The only way to get all this valuable information is to watch this urgent briefing. Click here to view it now.

In the meantime, I want to give you a sneak peak into one of my picks for Internet of Things megatrend that is already angling to dominate the market.

This company isn’t starting with fancy factories or self-driving cars. Rather, it’s bringing the IoT revolution to your local grocer.

Grocery store chains are rushing to embrace technology, according to a Bloomberg feature Monday. They’re motivated by one part modernization, two parts fear of an existential threat.

No matter the reasons, it’s an opportunity for investors.

Food retailing hasn’t changed much in 30 years. Bloomberg notes the last big innovation was barcode scanners.

In theory, attaching a universal scannable code to grocery items made them easier to track throughout the supply chain. But that doesn’t stop most retailers from expending a lot of human resources checking shelves.

To compensate, many companies are reaching out to start-ups that build shelf-scanning robots and self-checkout systems.

And now, Amazon.com (AMZN) is moving deeper into food retail. Not surprisingly, the rest of the industry is worried.

Amazon.com got in on the grocery-store game with its 2017 acquisition of Whole Foods. But it’s the company’s Amazon Go convenience stores that are set to spark a food-buying revolution.

Amazon Go’s 22 locations throughout the U.S. are completely cashier-free. Shoppers enter, pick up the items they need and leave. Cameras track what gets removed from shelves, and a digital bill is sent to the patron’s Amazon account as they exit.

The entire experience is frictionless. Can you say that about your last grocery-store run?

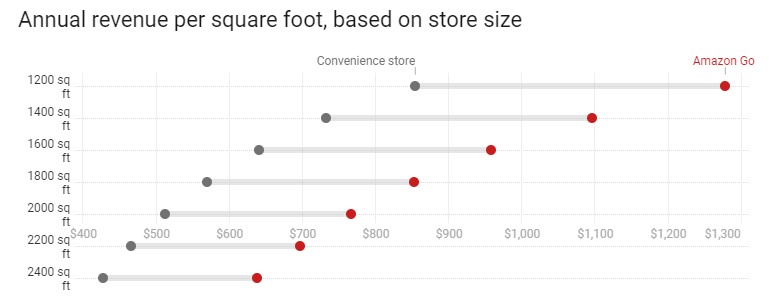

Privacy concerns aside, this kind of smart-shopping has big potential. Just 44% of the $900 billion U.S. grocery market goes to traditional stores. And the Seattle giant has its eye on the remaining 56%.

Amazon Go stores currently earn about 50% more revenue on average compared to a typical convenience store, according to global investment bank RBC. So that 56% isn’t really a pipe dream at all.

Amazon is an obvious play. But as you know, I think the less-obvious plays are more interesting. And there is a big hidden opportunity for investors in this grocery revolution: Sony (SNE).

You might think of televisions, PlayStations, cameras and car stereos when you think of Sony. But instead, envision all the components that make these electronic devices so sought-after …

The Japanese consumer electronics company has 50% market share in the sensors found in cameras, smartphones and commercial drones. Its scale, substantial intellectual property portfolio and best-in-class devices limit competition.

It’s in the best position to offer low-cost sensors needed in smartphones and applications.

And that’s a solid business plan …

After all, it’s simply more cost-effective for other companies to buy the sensors from Sony than build their own. This means nice profits for Sony.

Now, those sensors are finding use cases in Internet of Things applications.

With the right artificially intelligent software, millions of Sony imaging devices will move beyond recording to actually seeing the world.

Sony reported record second-quarter profits at the end of October. CFO Hiroki Totoki specifically cited strong demand for sensors and growing Internet of Things applications. He also reported that plans to build a new image sensor plant were finalized.

While the plans were initially laid in response to the demand for smartphone sensors, most of what it’ll be producing now will go toward IoT applications.

There is an interesting point of order potential investors should be aware of, though. Reuters reported in April that Daniel Loeb, a portfolio manager at Third Point LLC, has acquired a stake in Sony shares.

This is the second time in six years the activist investor assumed a large position in Sony. In the past, he has been a proponent of selling Sony Studios to create shareholder value.

Loeb’s firm, founded in 1995, targets event-driven, value-oriented investments.

This time, Loeb is targeting Sony’s sensor business.

Loeb is looking for Sony to drop the rope on its chips division and dedicate its time and resources to its entertainment divisions. He believes a buyout would be more profitable than continuing the status quo. Without the tech side, Sony would still have Sony Studios and its PlayStation video console franchise.

This is short-sighted thinking. And luckily, Sony isn’t taking the bait.

Sony knows the future of Internet of Things applications is in those sensors. And if they continue playing into this strength, they’ll dominate this market just like they did with smartphones.

With profits for its sensor division surging 59% to 76.4 billion yen, or roughly US$702 million, Sony has the leverage to argue against Loeb’s call.

In fact, profits from sensors have helped the stock break above $60.

Shares trade at 15.9x forward earnings for a market capitalization of $82.2 billion. That’s reasonable given the prospects for IoT.

Investors should look to any weakness as a buying opportunity.

Best wishes,

Jon D. Markman