Telemedicine is one of those face-palm ideas. Having doctors diagnose patients using videoconference technology is a no-brainer. It should be everywhere.

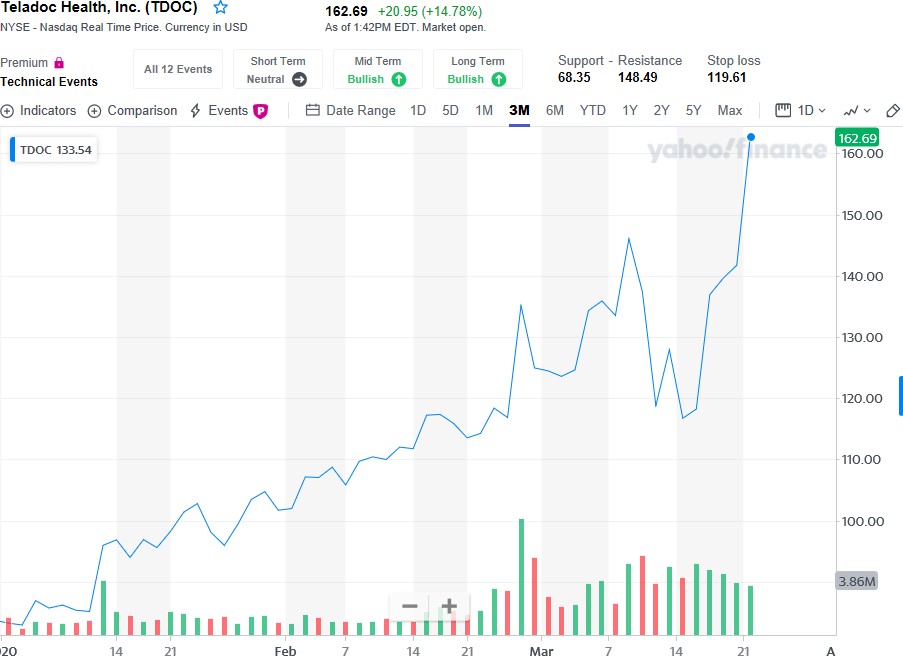

It turns out it took a global pandemic to make Teledoc (TDOC) a household name. The COVID-19 virus put the company’s shares atop the new high list. Investors are paying up to be a part of the story.

Modern telemedicine was born in 2001 when NASA wanted to find a way to provide extended healthcare to astronauts at the International Space Station. The challenge was otherworldly.

ISS is 239-foot-long spacecraft 220 miles away. More important, it’s a moving target flitting through the Earth’s lower orbit at 17,227 miles per hour. Thankfully, researchers had a running start.

In 1997, NASA sponsored the Medical Informatics and Technology Applications Consortium, a Yale University project operating out of Ecuador, Russia and the Artic. The goal was to commercialize telemedicine technology. Five years later Dr. Byron Brooks, an ex-NASA surgeon, and Michael Gorton, launched Teledoc.

The Dallas company had a simple business plan: Use advances in networking technology to provide on-demand remote medical care.

In 2015, Teledoc issued shares to the public at $19 apiece. Managers pitched institutional investors on the big opportunity of delivering on-demand, 24-hour healthcare via mobile devices, the internet, video and regular phone lines. The stock jumped 50% higher on opening day.

Since then, CEO Jason Gorevic has been on a buying binge. CrunchBase notes the company has completed 11 acquisitions with the aim of consolidating a fragmented market before larger companies with deeper pockets enter the telemedicine segment.

So far, the strategy is working like a charm.

Teledoc offers a scalable, fast-growing virtual healthcare platform with access to multi-specialty physician networks, from general medical and mental health to dermatology.

For 70 global insurers, 300 hospital systems and 40% of the Standard and Poor’s 500, the platform is critical to providing efficient and cost-effective healthcare.

According to a March investor presentation, sales have grown at a 55% compound average growth rate since 2015. During that time, revenues jumped from only $77 million to $553 million in 2019. For the current year, the firm is projecting sales of $703 million as Teledoc care providers oversee 5.7 million patient visits.

Many of those visits are referrals from health systems providers like UnitedHealth Group (UNH), Aetna (AET) and Premera Blue Cross, or large enterprises such as 3M Corp. (MMM), T-Mobile (TMUS) and Home Depot (HD).

These businesses are using Teledoc’s scale advantage to deliver up to 35% savings over in-person visits. The greater number of visits, the more savings derived.

Visitor growth is a key part of what Gorevic calls the company flywheel — a self-reinforcing loop made up of a few key initiatives. Together, they are very difficult to slow once the combination gains momentum. In the case of Teledoc those initiates are trust, quality user experiences and repeat visits.

The COVID-19 crisis has reinforced all three, and made the stock are big winner. Shares are up 60.9% in 2020, surging Friday to $141.74. Those gains seem likely to continue in the short term. A corporate press release noted that virtual visits were 50% higher during the week of March 13.

Related post: New Boom in Telecommuting Ushered in by COVID-19 Chaos

I first recommended Teledoc in 2018 at $66. At the time, I favored its Amazon.com-like business model.

That Teledoc is similar to Amazon also makes them a potential rival with the e-commerce giant, as they have future plans to enter the blossoming industry.

Amazon founder Jeff Bezos famously built a flywheel based on customer experience, platform traffic and third-party sellers. Great experiences led to increased traffic that attracted even more third-party sellers. Lower prices and more traffic followed.

Once that wheel began to spin, momentum kept it going.

Amazon.com, once merely an online destination for books, is now the biggest digital marketplace in the Western world. Third-party sellers have put millions of products only a click away.

The growth of the platform puts Amazon in an enviable position. Through December 2019, the company had an estimated 112 million Prime subscription members in the United States. They pay $119 annually for free shipping, streaming video, a limited digital music service and access to Prime Day member sales. They are also a fervent test audience for new Amazon products and services like Kindle, Alexa and Amazon Music.

Amazon Care was introduced last year. According to a CNBC report, the telemedicine service is currently available to Amazon employees in the Seattle area, but it may dovetail with the parent company’s larger healthcare ambitions.

In 2018, Amazon partnered with JPMorgan Chase (JPM) and Berkshire Hathaway (BRK) to address healthcare delivery, rising costs, insurance benefits and prescription drugs. Initially, Haven Healthcare will be in-house, providing care to U.S. based employees of the founding firms. Longer-term, the stated longer-term goal is to bring Haven innovations to other businesses.

While Teledoc is a wonderful business, investors should be aware Amazon is coming. Don’t chase shares higher. Buy pullbacks only.

Best wishes,

Jon D. Markman